Professional Tax is a direct tax levied by State Governments in India under the Constitution It applies to individuals earning income from employment, profession, trade, calling, or occupation. While the central government collects Income Tax, Professional Tax (PT) is collected by state governments as per their respective Acts.

In Karnataka, the tax is governed by the Karnataka Tax on Professions, Trades, Callings, and Employments Act, 1976, and is amended regularly through state budgets/notifications. PT must be deducted and paid to the government based on the applicable slab and statutory requirements.

Why Professional Tax Matters

PT is one of India’s most common statutory compliances required for almost every entity and individual engaged in economic activities in a state. If ignored:

- You face penalties, interest and compliance notices

- You risk enforcement action by State Commercial Tax officers

- You may lose credibility with regulators and bankers

In Karnataka, every working professional and business entity must evaluate whether they are liable to pay PT and register appropriately.

Professional Tax is collected by the State Government, not the Central Government.The oney is used for public services such as building roads and infrastructure, running government schools and colleges, improving hospitals and healthcare, supporting welfare schemes, and paying salaries and pensions of state government employees.

Who Is Liable to Pay Professional Tax in Karnataka?

1. Salaried Employees

If you are currently employed and earning a salary that exceeds the prescribed Professional Tax slab, your employer is legally required to deduct Professional Tax (PT) from your monthly salary and remit the deducted amount to the government within the specified timelines.

2. Employers / Businesses

All employers and registered business entities operating within the state of Karnataka are required to enroll under the Professional Tax Act and pay Professional Tax for their respective establishments. This mandatory requirement applies to the following categories:

- Companies (private/public limited)

- LLPs

- Partnership firms

- Sole proprietorships

- Associations, clubs, societies

- Co-operative societies

- Any business with fixed place of operation

These entities may also have to pay fixed yearly PT based on employee count or registration status.

3. Self-Employed Professionals

Individuals engaged in a profession or carrying on a business—such as doctors, consultants, lawyers, chartered accountants, freelancers, and similar professionals—may be required to pay Professional Tax on a yearly basis for their profession, provided they are actively engaged for a period exceeding the statutory limit prescribed during the financial year

4. Exemptions

Some categories are exempt, including:

- Senior citizens above a certain age

- Persons with specified physical disabilities

- Those with minimal time in practice (less than statutory days)

- Others as per government notification

Note: exact exemptions should be checked in the latest Karnataka PT schedule.

Karnataka Professional Tax Slabs (2025–26)

The Karnataka government has recently revised the Professional Tax (PT) slabs under the Karnataka Professional Tax Amendment Act, 2025, and the updated provisions have come into effect from 1st April 2025, making them applicable for the relevant assessment periods.

🧾 Salaried Individuals

| Monthly Income | PT to be Deducted |

| Up to ₹24,999 | Nil |

| ₹25,000 and above | ₹200 per month (standard) |

| In February (each year) | ₹300 |

The February PT deduction is ₹300 for salary above ₹25,000, while other months are ₹200 each.

This sets an annual maximum of ₹2,500 per employee.

Self-Employed / Professionals

If you are running a profession—such as a consultant, coach, chartered accountant, lawyer, doctor, training institute, or any similar professional activity—and you have been actively engaged in that profession for a period exceeding two years:

- PT is typically ₹2,500 per annum.

- Registration and payment are done online through the Karnataka PT portal (e-Prerana).

How to Register for Karnataka Professional Tax

All employers, self-employed professionals, and businesses are required to obtain a Professional Tax Enrollment Certificate (PT-EC) from the Karnataka Commercial Taxes Department.

Registration Procedure

The Karnataka Government has simplified the process using the e-Prerana online portal. Key steps:

- Visit the official PT portal:

Karnataka PT e-Prerana portal — ptax.karnataka.gov.in - Choose Registration Type:

- For professionals — use PAN

- For businesses — use GSTIN or PAN

- Enter details:

- Name, PAN/GSTIN, occupation, address

- OTP Verification:

OTP is sent to your mobile — verify and set password - Complete Profile:

Enter details of employees, business activities - Enrollment Certificate:

After registration you receive a certificate with a unique PT-EC number.

With the new e-Prerana system, PT enrollment is mostly instant, and payments & returns can be filed online anywhere.

Professional Tax Returns — Monthly & Annual

1. Monthly PT Returns

Employers are responsible for deducting Professional Tax (PT) from employee salaries on a monthly basis and are required to deposit the deducted amount with the government and file the applicable return on or before the 20th day of the following month

Example:

PT for April must be deposited & return filed by 20th May.

2. Annual Return (Form 5)

At the end of the financial year:

Employers are required to prepare a consolidated return that includes details of all Professional Tax (PT) deductions made for their employees during the year and must file this annual return on or before 30th April each year, as prescribed under the applicable regulations.

3. Business / Professional Returns

Entities holding a Professional Tax Enrolment Certificate (PT-EC) and not making any Professional Tax deductions from employees are required to file Form 4A on an annual basis to report the payment of fixed Professional Tax and formally close the compliance for the financial year.

4. Other Returns

There are specific monthly or quarterly Professional Tax statements, such as Form 5A, that employers are required to file, depending on factors like the number of employees on their rolls and the applicable Professional Tax payment schedule.

Payment Options & Due Dates

Payment Methods

✔ Professional Tax payments can be made through net banking facilities.

✔ Debit and credit cards are also accepted for making PT payments.

✔ Unified Payments Interface (UPI) can be used for quick and secure transactions.

✔ Payments may also be made through direct debit using the official online e-filing portal.

Due Dates

| Return Type | Due Date |

| Monthly PT Payment & Returns | 20th of the following month |

| Annual Return (Form 5) | 30th April every year |

| Form 4A Filing | Within 60 days from the close of the financial year |

Failure to comply with these prescribed timelines may result in the levy of penalties and applicable interest as per the provisions of the Professional Tax regulations.

Payment link- https://ptax.karnataka.gov.in/

PT Return- https://ptax.karnataka.gov.in/ptemployer

Due Dates

| Return Type | Due Date |

| Monthly PT Payment & Returns | 20th of next month |

| Annual Return (Form 5) | 30th April every year |

| Form 4A filing | Within 60 days of fiscal year close |

Adherence to these statutory due dates is mandatory. Any delay or failure in filing the returns or making payments within the specified timelines may attract penalties, interest, and other consequences as prescribed under the Professional Tax laws.

Penalties for Karantaka PT

Delays in payment or non-compliance with Professional Tax provisions can result in the following consequences:

1. Interest on Delayed Payment

✔ An interest charge of 1.5% per month is levied on the overdue Professional Tax amount.

✔ This interest is calculated from the original due date until the actual date of payment is made.

2. Penalty

✔ A penalty of up to 10% of the tax due may be imposed in cases of voluntary non-payment before the issuance of any official notice.

✔ In addition, separate late fees may be applicable for delayed filing of returns, such as ₹250 per month, subject to the limits prescribed under the rules.

3. Other Consequences

✔ Issuance of enforcement or demand notices by the Professional Tax Department.

✔ Initiation of legal proceedings against the business or employer in cases of continued or repeated defaults.

✔ Difficulties in obtaining future registrations, renewals, or facing increased scrutiny during departmental audits and inspections.

Common Scenarios & Practical Examples

Suppose Rohan works in Bangalore earning ₹35,000 per month.

✔ PT deducted: ₹200/month from April–January

✔ February deduction: ₹300

✔ March: ₹200

Total PT for year: ₹2,500.

Example 2: Small Business Employer

A company in Mysore with 8 employees needs to:

✔ Register for PT-EC

✔ Pay ₹1,500 per year as employer PT

✔ Deduct PT from employees satisfying the slab

✔ File monthly returns and annual return

Example 3: Freelancer / Consultant

Seema is a graphic designer with PAN and no employees:

✔ She must enrol using her PAN

✔ Because she’s self-employed more than two years, she pays ₹2,500 per annum

✔ File her annual report on the portal

Example 4: Company With GST but No Revenue

Even if a company has no active operations or revenue but holds GSTIN, PT may be applicable. Courts and practitioners often advise filing returns and payments or surrendering GST if dormant. (Reddit community experiences show confusion when companies miss PT despite inactivity.)

As per Slab I have created the Karantak PT deduction formula

=IF(B2<25000,0,IF(OR(C2=”Feb”,C2=”February”),300,200))

- Put salary in B2

- Put month name in C2

- Put formula in D2

- Drag down for all employees

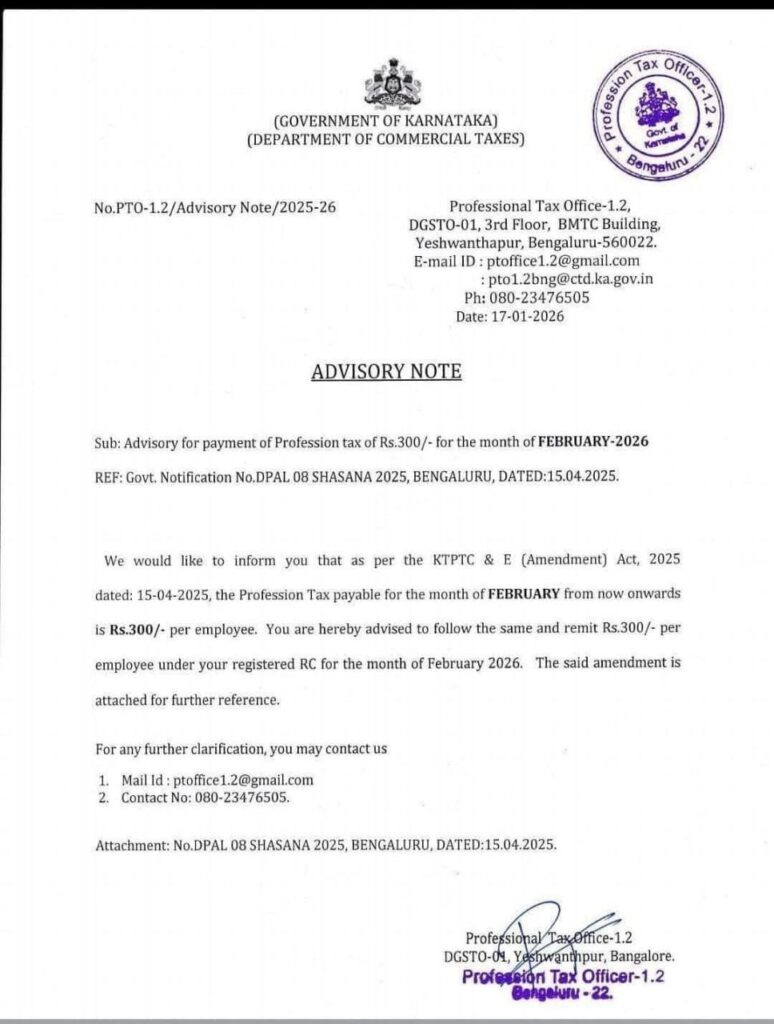

Notification on Jan 2026

**mitolyn**

Mitolyn is a carefully developed, plant-based formula created to help support metabolic efficiency and encourage healthy, lasting weight management.

ah88 https://www.adah88.net

I’ll immediately grab your rss as I can not in finding your e-mail subscription link or newsletter service. Do you’ve any? Kindly let me understand so that I may subscribe. Thanks.

Great beat ! I would like to apprentice even as you amend your web site, how could i subscribe for a weblog web site? The account aided me a acceptable deal. I had been tiny bit familiar of this your broadcast offered shiny transparent idea

어제 친구들과 회식 자리로강남가라오케추천다녀왔는데, 분위기도 좋고 시설도 깨끗해서 추천할 만했어요.

요즘 회식 장소 찾는 분들 많던데, 저는 지난주에강남가라오케추천코스로 엘리트 가라오케 다녀와봤습니다.

분위기 있는 술자리 찾을 땐 역시강남하퍼추천확인하고 예약하면 실패가 없더라고요.

회사 동료들이랑강남엘리트가라오케방문했는데, VIP룸 덕분에 프라이빗하게 즐길 수 있었어요.

신논현역 근처에서 찾다가강남룸살롱를 예약했는데, 접근성이 좋아서 만족했습니다.

술자리도 좋지만 요즘은강남셔츠룸가라오케이라고 불릴 만큼 서비스가 좋은 곳이 많더군요.

sjyd4g

Enjoyed studying this, very good stuff, thanks. “The hunger for love is much more difficult to remove than the hunger for bread.” by Mother Theresa.

treasury casino brisbane

References:

https://bandori.party/user/585256/rockquiet48/

Slot tại link 66b có tính năng “turbo mode” – quay nhanh gấp đôi, phù hợp với người thích tốc độ. TONY03-13H

ProDentim is a distinctive oral-care formula that pairs targeted probiotics with plant-based ingredients to encourage strong teeth, comfortable gums, and reliably fresh breath.

Boostaro is a purpose-built wellness formula created for men who want to strengthen vitality, confidence, and everyday performance.

HeroUP is a premium mens wellness formula designed to support sustained energy, physical stamina, and everyday confidence.

Mitolyn is a carefully developed, plant-based formula created to help support metabolic efficiency and encourage healthy, lasting weight management.

PurDentix is a revolutionary oral health supplement designed to support strong teeth and healthy gums. It tackles a wide range of dental concerns

AquaSculpt is a high-quality metabolic support supplement created to help the body utilize fat more efficiently while maintaining steady, reliable energy levels throughout the day.

Maintaining prostate health is crucial for men’s overall wellness, especially as they grow older. Conditions like reduced urine flow, interrupted sleep

Gluco6 is a natural, plant-based supplement designed to help maintain healthy blood sugar levels.

InsuLeaf is a high-quality, naturally formulated supplement created to help maintain balanced blood glucose, support metabolic health, and boost overall vitality.

Arialief is a carefully developed dietary supplement designed to naturally support individuals dealing with sciatic nerve discomfort while promoting overall nerve wellness.

Manergy is an advanced male vitality supplement created to help support healthy testosterone levels

NerveGenics is a naturally formulated nerve-health supplement created to promote nerve comfort, cellular energy support, antioxidant defense

ProstAfense is a premium, doctor-crafted supplement formulated to maintain optimal prostate function, enhance urinary performance, and support overall male wellness.

Nitric Boost Ultra is a daily wellness formula designed to enhance vitality and help support all-around performance.

NerveCalm is a high-quality nutritional supplement crafted to promote nerve wellness, ease chronic discomfort, and boost everyday vitality.

Prosta Peak is a high-quality prostate wellness supplement formulated with a comprehensive blend of 20+ natural ingredients and essential nutrients to support prostate health

Kerassentials is an entirely natural blend crafted with 4 potent core oils and enriched by 9 complementary oils and vital minerals.

NativeGut is a precision-crafted nutritional blend designed to nurture your dog’s digestive tract.

Prostadine concerns can disrupt everyday rhythm with steady discomfort, fueling frustration and a constant hunt for dependable relief.

The bodys natural process of skin cell renewal is essential for preserving a smooth, healthy, and youthful-looking complexion.

Prosta Peak is a high-quality prostate wellness supplement formulated with a comprehensive blend of 20+ natural ingredients and essential nutrients to support prostate health

GL Pro is a natural dietary supplement formulated to help maintain steady, healthy blood sugar levels while easing persistent sugar cravings.

Visium Pro is an advanced vision support formula created to help maintain eye health, sharpen visual performance, and provide daily support against modern challenges such as screen exposure and visual fatigue.

ViriFlow is a dietary supplement formulated to help maintain prostate, bladder, and male reproductive health. Its blend of plant-based ingredients is designed to support urinary comfort and overall wellness as men age.

AquaSculpt is a high-quality metabolic support supplement created to help the body utilize fat more efficiently while maintaining steady, reliable energy levels throughout the day.

MounjaBoost is a next-generation, plant-based supplement created to support metabolic activity, encourage natural fat utilization

GL Pro is a natural dietary supplement formulated to help maintain steady, healthy blood sugar levels while easing persistent sugar cravings.

NativeGut is a precision-crafted nutritional blend designed to nurture your dog’s digestive tract.

Backbiome is a naturally crafted, research-backed daily supplement formulated to gently relieve back tension and soothe sciatic discomfort.

This was a helpful and interesting read. I appreciate when an article honors the reader’s time while still offering substance, and I’m glad you published it.